Sauron case hinges on ‘certified’ insurance policy; general public cannot buy certified policies

TN revenue department illegally forces motorists to buy policies that don't meet standard making them suitable as 'proof of financial responsibility'

CHATTANOOGA, Tenn., Friday, Dec. 6, 2024 – It’s hard to believe, but state of Tennessee has assigned its attorney general Jonathan Skrmetti to defend its open criminal program of “mandatory insurance,” a criminal shakedown of the public

His office has already filed a motion against the people in my newly filed federal fraud suit against revenue Cmsr. David Gerregano. The attorney’s name is Nick Barco.

In the state administrative case – after 16 months of litigation in a separate case in agency and many filings – the legal “nut” or core comes down to the concept of certification. If I am truly compelled to “get insurance” to use the public road, what sort of evidence do I get from the insurance company that meets the legal requirement of “proof of financial responsibility,” or POFR?

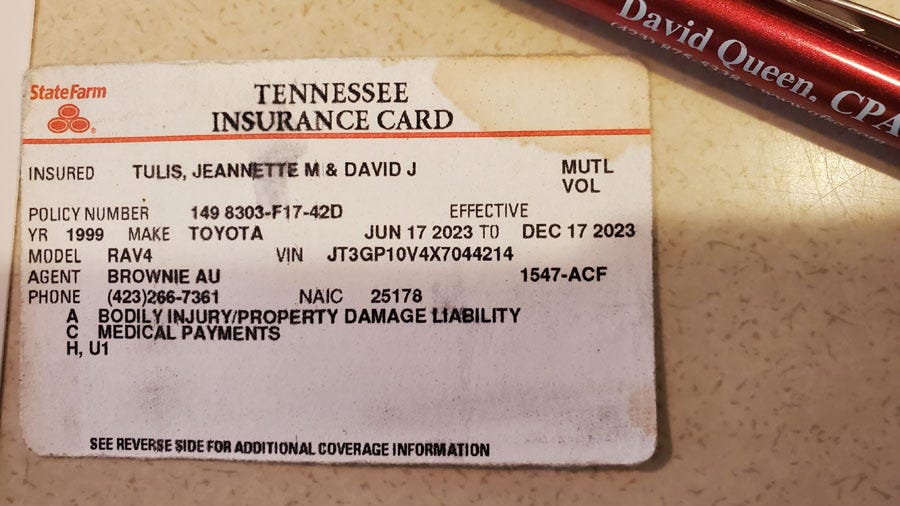

Is my declarations page in my glovebox enough? Is my billfold card legally sufficient?

The point I raise today in the mind of administrative hearing judge Brad Buchanan, in a 40-minute oral argument, is that of legal sufficiency.

That may not sound like a big deal. But does my printout from Grange or the tag from State Farm meet the law’s requirements? And, if I don’t have this paperwork, is that a crime?

The answer is no, and the observations I make today are, for me, a pack of data reassembled from all my filings and making things super clear.

That’s why I demanded oral argument, to get to the heart of the conflict with less relevant or dispositive material left out.

What is certification?

To certify means to guarantee as proof. The word comes from the word “certain.” That means absence of doubt. Black’s Law Dictionary says a certificate is a ticket, a warrant, by form constituting “evidence of truth of the facts stated therein.”

A certified birth certificate is better than a mere copy of your birth certificate. A certified letter is more sure to have proveably arrived than regular first class. A certified document is more secure , more binding, more sure than other documents in a world of paper and digital files. It has higher validity, more substance to merit trust. It’s a paper sworn or notarized, and has higher value even if not sworn or notarized.

Financial responsibility law & the ‘certified policy’

The case David Jonathan Tulis v. department of revenue, whichever of the three you might refer to, turns on whether I and millions of other people in Tennessee are obligated to get “non-certified” motor vehicle insurance policies.

The law clearly obligates a tiny group of people to get “certified” policies. Do the rest of us have to follow along to get “uncertified” policies?

Revenue is so keen on keeping up its fraud it is willing to allow 40,800 people a year to be criminally convicted and impose untold misery upon the public, almost always poor people who choose grocery, heat and car repairs over auto insurance.

DOR in its “Eye of Sauron” for electronic insurance verification (EIVS) surveils all state motor vehicle registrants for insurance noncustomers. It tags them with a 4-notice sequence of mail ending with tag revocation without a hearing.

What follows gets into the nitty gritty of Tennessee law. If you are looking in from another state, or are a Tennessean wanting to join the fight for Christian liberty and constitutional restraint on deputies and cops, this report is a primer.

It teaches you to spend time reading the state law, in detail and in the broad scope of any part of it. Once you slowly, patiently, spend time in it will allow “problems” with a state actor practices come into view.

Certified policies key in case

All provisions below are in T.C.A. 55, chapter 12, unless otherwise noted. Note the word certified.

T.C.A 55-12-102 Definition of “motor vehicle liability policy’

(7) “Motor vehicle liability policy” means an “owner’s policy” or “operator’s policy” of liability insurance, certified as provided in § 55-12-120 or § 55-12-121 as proof of financial responsibility [POFR], ***.”

119 – This law is about “manner of proof” of POFR

Proof of financial responsibility, when required under this chapter with respect to a motor vehicle or with respect to a person who is not the owner of the motor vehicle, may be given by filing: (1) A certificate of insurance as provided in § 55-12-120.

Notice POFR is not universal, but “when required.” Notice here a “certificate of insurance” from an insurance company. Regular members of the public buy insurance, not no such person gets a “certificate.”

A court case, backs up this analysis. The summary: “Fact that liability policy was on file and approved by Commissioner of Insurance and Banking did not make policy a “certified policy” under financial responsibility statute. T.C.A. §§ 56-603, 59-1201 to 59-1240. McManus v. State Farm Mut. Auto. Ins. Co., 1971, 463 S.W.2d 702, 225 Tenn. 106. Insurance 2737. Just because a policy exists, or is noted on a data file in department of insurance, doesn’t mean it’s proof of financial responsibility.

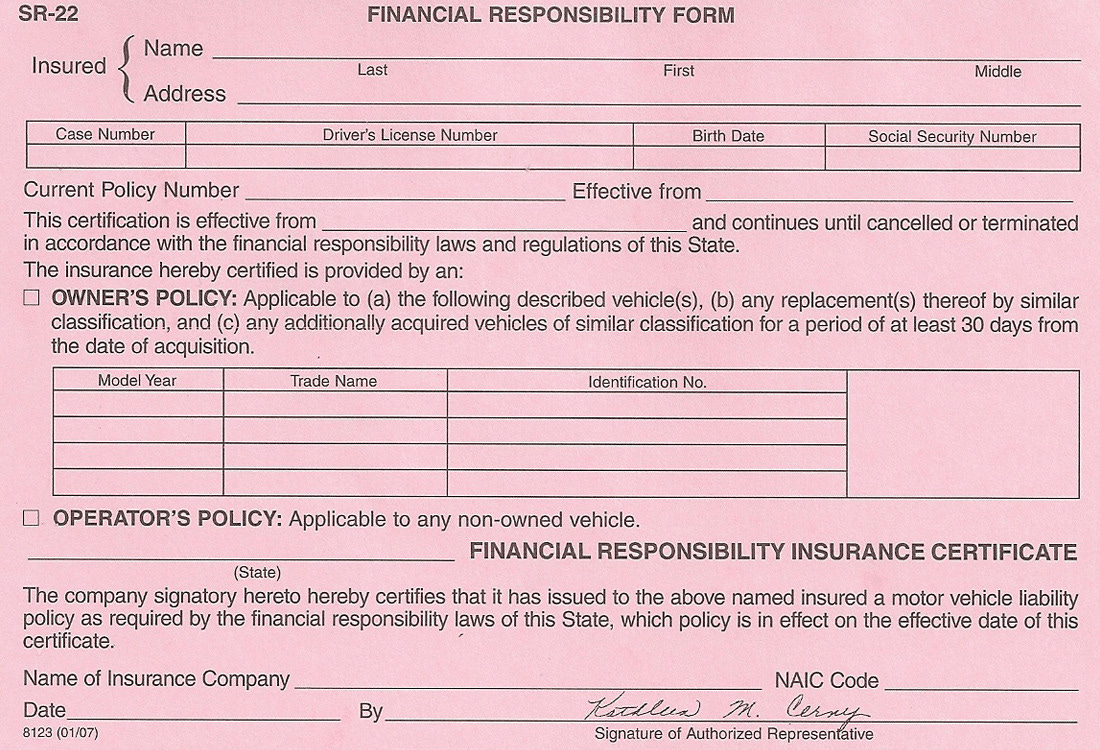

120. Certificates and certification [ SR-22 ]

Notice again, “written certificate” of an “insurance carrier” that “certifies” existence of a policy. Tennessee requires SR-22 insurance for high-risk, the term belonging to industry.

Proof of financial responsibility may be furnished by filing with the commissioner [of safety] the written certificate of any insurance carrier duly authorized to do business in this state, certifying that there is in effect a motor vehicle liability policy for the benefit of the person required to furnish proof of financial responsibility. This certificate shall give the effective date of the motor vehicle liability policy, which date shall be the same as the effective date of the certificate, and shall designate by explicit description or by appropriate reference all motor vehicles covered thereby, unless the policy is issued to a person who is not the owner of the motor vehicle.

121. Nonresidents; certificates and certification

A nonresident may give proof of financial responsibility by filing with the commissioner a written certificate or certificates of an insurance carrier licensed to transact business in the state[.] ***The commissioner shall accept the certificate upon condition that the insurance carrier complies with the following provisions with respect to the policies so certified.”

123. This section’s is “Cancellation or termination of policies; notice.”

When an insurance carrier has certified a motor vehicle liability policy under § 55-12-120, insurance so certified shall not be cancelled or terminated until at least ten (10) days after notice of cancellation or termination of the insurance so certified shall be filed with the commissioner, except that such a policy subsequently procured and certified shall, on the effective date of its certification, terminate the insurance previously certified with respect to any motor vehicles designated in both certificates.”

Exciting fact: a person with suspended licensed has the privilege restored on condition of insurance. He cannot be revoked without a 10-day notice by the insurer to safety. Ordinary policies among those of 40,800 people convicted annually for “no insurance” do not get a notice. When my policy lapsed on my disputed minivan, State Farm did not send notice under this section.

124. Policies required by other law

This section refers to policies required to be held by people in trucking. If such policy is certified, it can become POFR. The process is if “certified” it becomes “proof of financial responsibility under this part.

(a) This part shall not be held to apply to or affect policies of automobile insurance against liability that may now or hereafter be required by any other law of this state, << motor carriers>> and such policies, if they contain an agreement or are endorsed to conform with the requirements of this part, may be certified as proof of financial responsibility under this part.

126. This section is described as “maintenance of proof; suspension of license and registration.”

Support princely combat v. principalities & powers

This contains key phrase, “financial responsibility certificate.” In the scam, cops just ask for “insurance.” They can only use the Eye of Sauron verification system upon such “FR certificate” mentioned here.

(a) Except for suspensions under § 55-12-115, and the proof required as provided in § 55-12-114, a person who is required to provide proof of financial responsibility shall maintain that proof for the period of the revocation or suspension. If a person elects to use a policy of insurance and financial responsibility insurance certificate as proof of financial responsibility under this section, then the effective date on the financial responsibility certificate is the date upon which financial responsibility was proven, and financial responsibility must be maintained for the period of the suspension or revocation.

133 Safety shall consent to cancellation of any certificate of insurance if there is an alternate POFR.

136 certificates are within corporate infrastructure of the law. Insurance companies in the nonprofit club of TFRL participants have a “certificate of authority.”

139. Officers can run only certified policies in scene of accident. T.C.A. 55-12-139 (b)(1)(A) says, “At the time a driver of a motor vehicle is charged ***, an officer shall request evidence of financial responsibility as required by this section.” The word evidence indicates the officer is authorized to obtain “proof,” again, a certified evidence of responsibility, that being the SR-22 form.

Certificates also appear in the first sentence of 139, which the department claims makes POFR mandatory on all. It says, “(a) This part shall apply to every vehicle subject to the registration and certificate of title provisions.”

A certificate of title is a proof of ownership, not just a piece of paper or a report of ownership, but a sure representation, a legal certainty connecting an owner to an automobile or motor vehicle, beyond any doubt. A certificate of title is said to be prima facie evidence of ownership.

210. DOR’s whole program hangs on its interpretation of 210. The Westlaw description is Uninsured motor vehicles; notice to owner; failure to provide proof of insurance; fees and penalties.

This provision supports my argument that EIVS is to surveil only certified policies, or SR-22 policies.

(g) If the vehicle is no longer insured by the automobile liability insurer of record and no other insurance company using the IICMVA model indicates coverage after an unknown carrier request under § 55-12-205(3), the owner of the motor vehicle becomes eligible for notice as described in subsections (a) and (b).

Key words in this section are “ automobile liability insurer of record” and “eligible for notice.” Holders of regular polices don’t do business with an insurer of record. They just buy insurance 0n the free market. Only a person who let’s an obligatory certificated policy laps is “eligible for notice.”

212. Program certification and implementation

The program shall be installed and fully operational upon certification by the commissioner of revenue that the program has been successfully tested and is ready for implementation, but not later than January 1, 2017. Until such certification occurs, no law enforcement action shall be taken based on the program.

This provision provides a crucial point in our lawsuit. The program was “certified” before it went live Jan. 1, 2017. I am asking hearing officer Brad Buhanan to “decertify” the program to halt its operation until the department reorganizes financial responsibility in accordance with law.

Here’s the killer

55-10-108. Miscellaneous provisions

State law makes distinction between insurance policies held by the public, and certified policies that are legally sufficient to be “proof of financial responsibility.” This section is a killer. I’ve added paragraphs so you can see what’s happening.

Any motor vehicle officer investigating any accident, at the time of and at the scene of the accident, may have the parties exchange insurance information, which would include the name of each party’s insurance company and the location of an agency of the insurance company.

Notice, this is ordinary insurance

Reports prepared by a law enforcement officer shall include information pertaining to the insurance policy, including the name of the insurance company, if known, of each person involved in the accident.

Again, ordinary insurance. Watch the next sentence. Keep both eyes open on this baby:

If a person has a certificate of compliance with the Tennessee Financial Responsibility Law of 1977, compiled in chapter 12 of this title, issued by the commissioner of safety, a copy of the certificate shall be included in the report.

Tenn. Code Ann. § 55-10-108 (emphasis added)

Notice the law sees the SR-22 as issued by the commissioner of safety. This insurance is not the policy in paragraphs 1 and 2. Graph 3 speaks of a different animal — the certified motor vehicle liability insurance policy described in 102, definitions.

Support David directly by U.S. mail, David Tulis c/o 10520 Brickhill Lane, Soddy-Daisy, TN 37379, or via GiveSendGo at this link.