Journalist urges comptroller probe of ‘mandatory auto insurance’ scam

$65,000 'cash deposits' are treasury department tripwire into probing rogue "Eye of Sauron" surveillance defying TN law I am suing to protect

My second report to the Tennessee comptroller of the treasury, Jason Mumpower, is sent by first-class U.S. mail June 26, 2024, seeking intervention of a state office that accounts for all the stray pennies and is charged with investigating fraud, misfeasance and malfeasance.

I attempt to draw Mr. Mumpower into action by focusing on a tiny detail likely to stir the brainpower of a bean counter. The detail is uncovered in David Jonathan Tulis v. Department of Revenue, a case lodged a year now in administrative court seeking to end a mass fraud and public extortion racket run by David Gerregano, commissioner of revenue.

It deals with two cash deposits of F$65,000. Now, let the mystery begin to unfold.

***

Dear Mr. Mumpower,

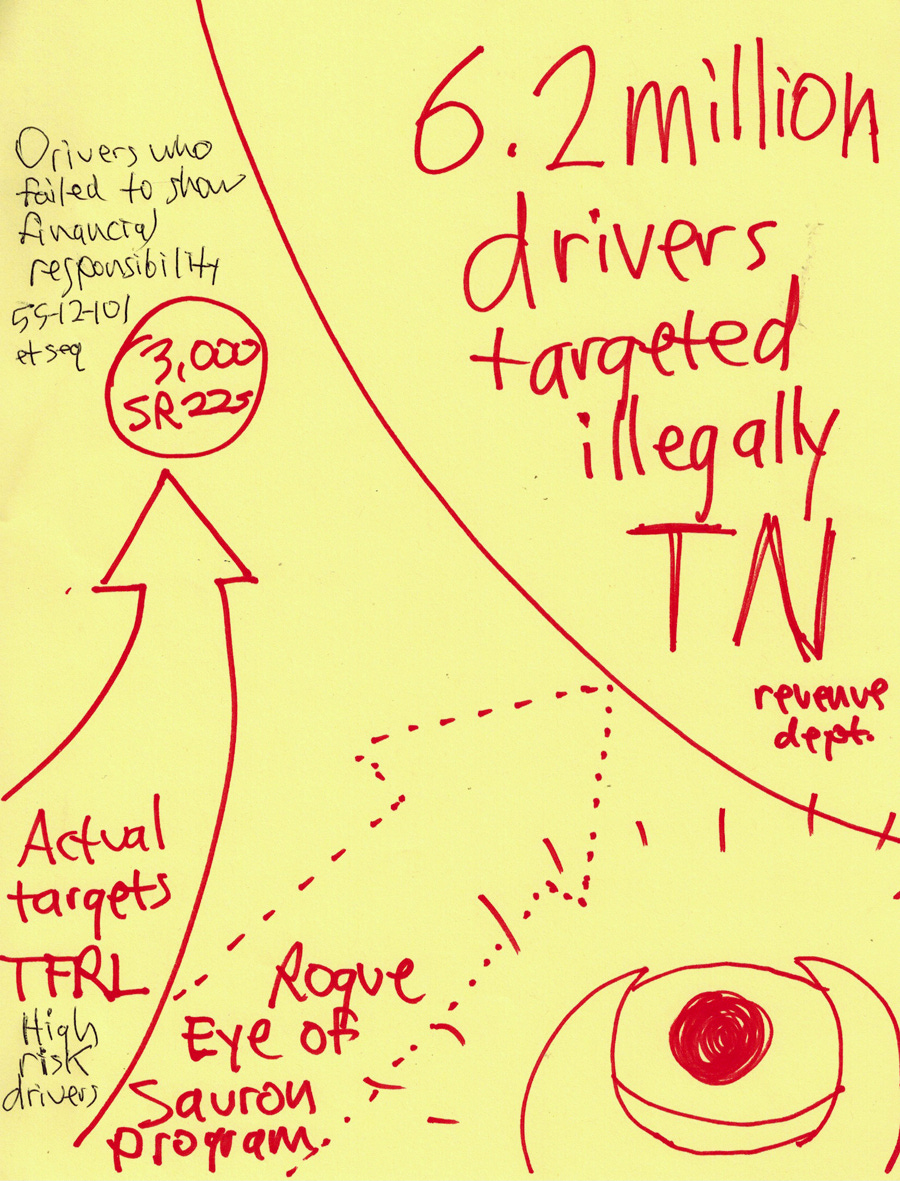

I’m the investigative reporter who wrote you July 27, 2023, as I was entering into a contested case with the department of revenue challenging its misuse of T.C.A. § 55-12-201, also known as the Atwood law or the electronic insurance verification system, EIVS. The system is intended to monitor about 3,000 scofflaws of the Tennessee financial responsibility law of 1977 who agree to carry insurance up to 5 years as a condition of restoring suspended licenses and tags. Using EIVS, however, DOR corruptly and illegally forces “mandatory insurance” upon 6.34 million members of the traveling public as a whole, with 408,800 criminal convictions — most all among the indigent — in a 5-year period under color of TFRL, sect. 139.

The Eye of Sauron program, as I call it, is official misconduct and corruption of the state government serving private and corporate interests, and injuring the whole citizenry.

I will be deposing DOR official Jennifer Lanfair July 9 in Nashville and asking questions that the comptroller of the treasury should be asking. I suggest you send a representative to the 9 a.m. encounter in David Jonathan Tulis v. Department of Revenue, Docket no. 23-004.

A tiny but suggestive detail in this sprawling fraud is the banking of $65,000 “deposits of cash” under the TFRL and under Atwood that the department collects under its policy administering the tail end of the TFRL.

I say “tail end” because safety is the moving party in administration of the law, and DOR is the tail. DOR doesn’t collect cash bonds in lieu of insurance when a motorist after a crash complies with TFRL. Safety does.

DOR says people, absent any qualifying crash, may use the public road only if they have insurance, buy a bond or send the department a $65,000 cash deposit.

DOR says I might opt to buy $65,000 bond for my uninsured personal conveyance if I want to enjoy ingress and egress liberties. Such bonds are nowhere available. Nor do I have $65,000 for a cash deposit to buy access to the road open and free to me and all other citizens of like station as a matter of right, acting outside the privilege.

The program uses state authority under color of law to extort $1 billion or more a year in premiums from the public to benefit 350 insurance companies. That such project is outside the law, as I am showing in our case, is evidenced in two $65,000 payments made by others that disturb the illusion of propriety and compliance.

After a qualifying accident that makes a person subject to the law, a party must show financial responsibility in any of four ways.

(b) The following, and only the following, shall be acceptable proof of financial security:

(1) Filing of written proof of insurance coverage with the commissioner on forms approved by the commissioner;

(2) The deposit of cash with the commissioner [of safety] of no less than the amount specified in § 55-12-102, or in the total amount of all damages suffered, whichever is less, subject to a minimum deposit of one thousand five hundred dollars ($1,500);

(3) The execution and filing of a bond with the commissioner of no less than the amount specified in § 55-12-102, or in the total amount of all damages suffered, whichever is less, subject to a minimum bond of one thousand five hundred dollars ($1,500); or

(4) The submission to the commissioner of notarized releases executed by all parties who had previously filed claims with the department as a result of the accident.

55-12-105. Deposit of security; proof of security

First of all, notice how uninsured parties may remain compliant with the law. We are not a mandatory insurance state, and no one is required to become an insurance industry customer to use the roads, or to be coerced into buying insurance. Uninsured parties who have an accident can settle the dispute among themselves without insurance, and option No. 4 shows they can use their cars sans insurance without running afoul of the TFRL. “The submission to the commissioner of notarized releases executed by all parties who had previously filed claims with the department as a result of the accident.”

Such parties are compliant to the law, are uninsured and yet the state uses its police power to arrest them and seize their cars and harass them and eat out their substance if they don’t show a bond or insurance certificate.

DOR and EIVS surveil these uninsured people and revoke their registrations.

My focus in this letter is on § 55-12-105 No. 2. The cash deposit in No. 2 is paid to the commissioner of safety. He puts the money with the state treasurer and draws from the amount to pay out the motor vehicle accident victim. (Option No. 3, a financial bond, is not available ahead of any accident, according to my market research.)

In no way is a cash deposit in No. 2 higher than the cost to reimburse an accident victim. “(b) In no case shall security be required that is greater in amount than that specified in § 55-12-102, and in no event shall this security be in an amount less than five hundred dollars ($500).” § 55-12-110. Damages; amount of security

Safety is authorized to receive the cash deposit up to $65,000 as follows.

(a) Any money deposited with the commissioner [of safety] in compliance with the requirements of this chapter shall be deposited by the commissioner in the custody of the state treasurer, and shall be applicable only to the payment of a judgment or judgments rendered against the person making the deposit or the person in whose behalf the deposit was made. The commissioner is authorized to pay out of any funds deposited in compliance with the requirements of this chapter, the amount of any final judgment returned against the party making the deposit or the person in whose behalf the deposit was made, upon receipt of a certified copy of the final judgment.

(b) After expiration of one (1) year from the date of the accident for which deposit has been made, the commissioner shall, upon receipt of a sworn statement of the party making the deposit that no court action has been brought as a result of the accident for which the deposit was made, return the deposit to the person making the deposit. Should the commissioner have reason to believe that this sworn statement is not true, additional proof may be required to substantiate the statement as the commissioner considers necessary.

55-12-112. Deposits

The funds that safety receives are dispersed in short order. The deposit is to satisfy an accident. It “shall be applicable only to the payment of a judgment or judgments rendered against the person making the deposit.” Safety is authorized to “pay out of any funds deposited in compliance with the requirements of this chapter.” Any surplus is “returned against the party making the deposit or the person in whose behalf the deposit was made, upon receipt of a certified copy of the final judgment.” Safety holds on to the money up to a year. If no suit for damages is filed and no settlement made, safety returns the cash deposit (by check, presumably) to the sender “upon receipt of a sworn statement of the party making the deposit that no court action has been brought as a result of the accident for which the deposit was made.”

The illegal act the law identifies is DOR’s Cmsr. Gerregano’s receiving cash bond payments outside “the requirements of this chapter.” He may, or may not, deposit the money “in the custody of the state treasurer” — but on what authority?

$65,000 ‘cash deposit’

I will explore this matter of receiving, holding and disbursing the money in deposition. I ask you, sir, are you disturbed at what I’m finding?

The official corruption of receiving payments outside of statute I expose in my case and in my reporting is this: Cmsr. Gerregano is banking funds he is nowhere authorized to receive. He is extorting the public, acting outside the scope of the law, and injuring me and hundreds of thousand Tennessee citizens.

Bizarre situations appear as Gerregano policy defeats clear law. If either of the 2 cash deposit payors has a $15,000 qualifying accident, and is not insured, must he put up $15,000 with the commissioner of safety even though commissioner of revenue has $65,000 he paid earlier? Would the $15,000 be drawn from the $65,000 on deposit with revenue? No provision exists for DOR to settle up with an injured accident party from its $65,000 pot. The payor is not free to not have to pay safety the cash deposit of $15,000 in his accident. That is double payment. That is violation of due process, and violation of equal and fair treatment under law.

Other questions about these DOR cash deposits, Mr. Mumpower. Does the money draw interest? Who gets it? If the payor gets it, does DOR report the interest to IRS? Does the payor get an annual report of the cash held by DOR? What if the payor dies? How does he get the money back? What is the legal nature of such payment? What are the protocols?

No doubt my deposition will uncover some of the corrupt practices connecting with Atwood and TFRL, including this one, which is a mere detail.

I have been investigating this departmental fraud for a year. Eye of Sauron abrogates or nullifies more than 20 provisions in TFRL in addition to violating the clear spirit and intent of the law, its moral purpose.

DOR alleges, despite court cases regarding financial responsibility, that all registered vehicle owners are irresponsible, high-risk, dangerous and evil and must at all times be able to show proof of financial security, though no crash has occurred among any one of them for which they must show financial responsibility. The program is an institutionalized crime of oppression. It is official corruption, violation of clear law in the interest of at least one Bill Lee appointee and of the insurance companies that secure a captive clientele.

Sir, I put you and your office on notice about these law violations. Please do your part to end injurious practices getting an overdue public airing.

Guarded reply